U.S. Plumbing Industry Statistics: Costs, Demand & Trends (2026)

The U.S. plumbing industry is a foundational part of the national economy, supporting residential housing, commercial construction, and critical infrastructure. As of 2026, the sector reflects steady demand driven by aging buildings, population growth, and ongoing maintenance needs across all regions. This dataset examines industry size, service costs, workforce dynamics, and long-term trends shaping plumbing services in the United States.

U.S. Plumbing Industry

The U.S. plumbing industry is a large, essential service sector that supports residential housing, commercial buildings, and public infrastructure nationwide. Entering 2026, plumbing demand remains resilient due to the ongoing need for system maintenance, repairs, and upgrades across both new and aging properties.

Industry data shows that plumbing services represent a significant share of the construction and facilities services economy, with activity spanning small local contractors to large commercial operators. Unlike discretionary home services, plumbing work is non-optional, mainly making the industry less volatile during economic slowdowns.

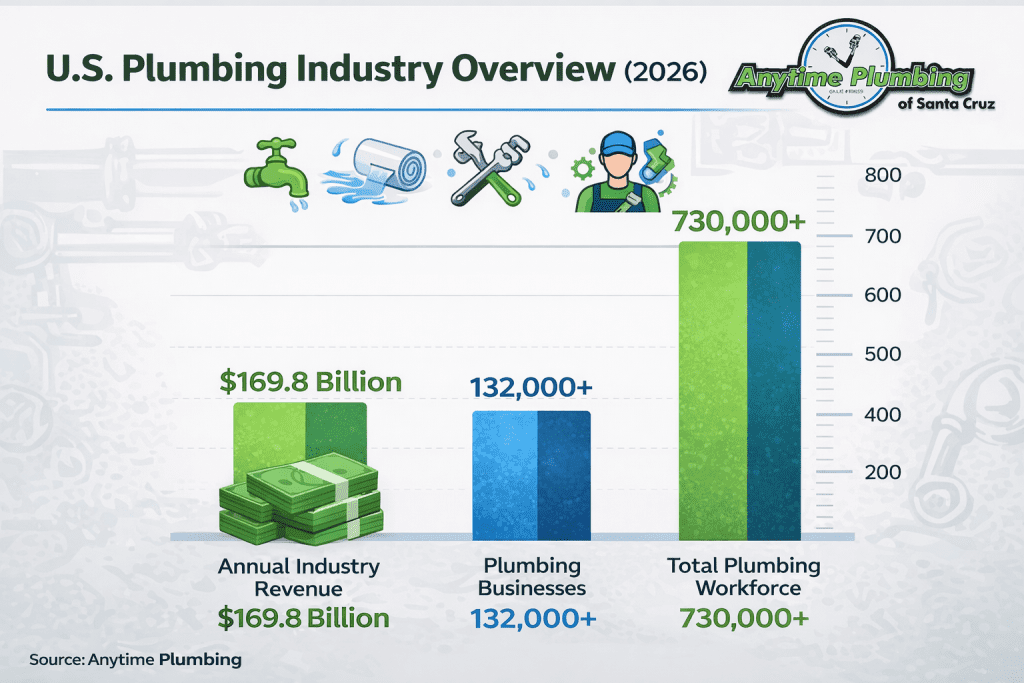

Key overview statistics for the U.S. plumbing industry:

- The U.S. plumbing industry generates over $160 billion in annual revenue, placing it among the most significant skilled trades in the country.

- More than 130,000 plumbing businesses are operating across the United States, most of which are small, independently owned firms.

- The industry employs over 700,000 workers, including licensed plumbers, pipefitters, and related trades.

- Commercial and nonresidential projects account for the majority of industry revenue, while residential plumbing drives a high volume of service calls.

- Demand is supported by aging housing stock, infrastructure replacement, and ongoing construction activity in both urban and suburban markets.

- Plumbing services remain essential year-round, with limited exposure to seasonality compared to other home service trades.

U.S. Plumbing Market Size & Growth

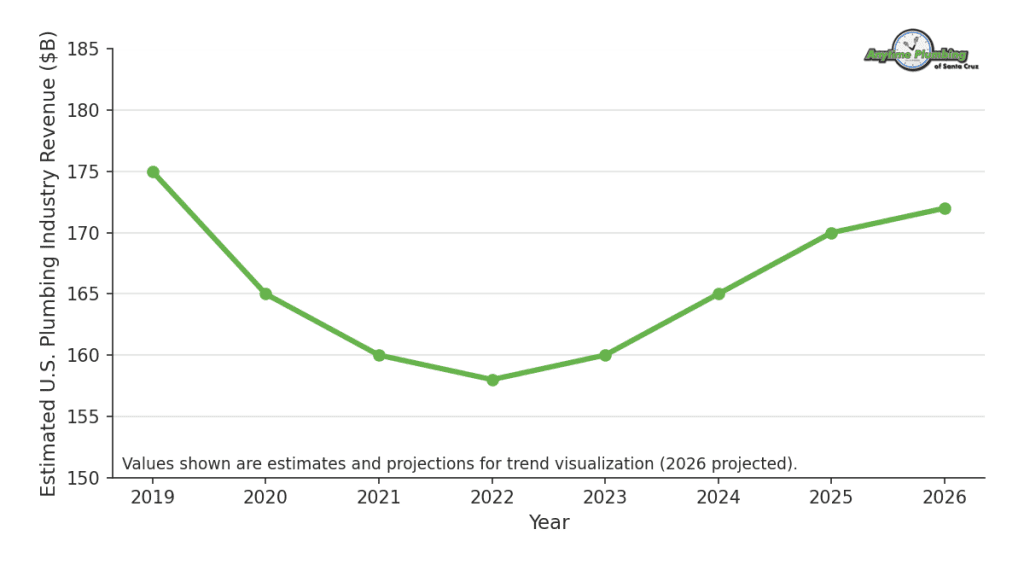

The U.S. plumbing market has shown steady, long-term growth driven by construction activity, infrastructure investment, and ongoing repair demand. By 2026, the industry will continue to expand at a stable pace, supported by both residential housing needs and commercial development.

Unlike cyclical construction segments, plumbing benefits from a mix of new construction and recurring service work, helping smooth revenue volatility across economic cycles. Stricter building codes, water-efficiency standards, and the modernization of older systems also reinforce market growth.

Key market size and growth indicators:

- The U.S. plumbing industry is valued at approximately $170 billion, reflecting consistent year-over-year expansion.

- Industry revenue growth has averaged 2–3% annually, aligning with broader construction and facilities maintenance trends.

- Residential plumbing remains the largest-volume driver, while commercial and institutional projects deliver higher per-project revenue.

- Infrastructure upgrades, including pipe replacement and system retrofitting, represent a growing share of market activity.

- Demand remains resilient even during economic slowdowns, as plumbing services are non-discretionary.

- Long-term growth is supported by population growth, housing turnover, and the nationwide aging building stock.

Demand for Plumbing Services (Residential vs Commercial)

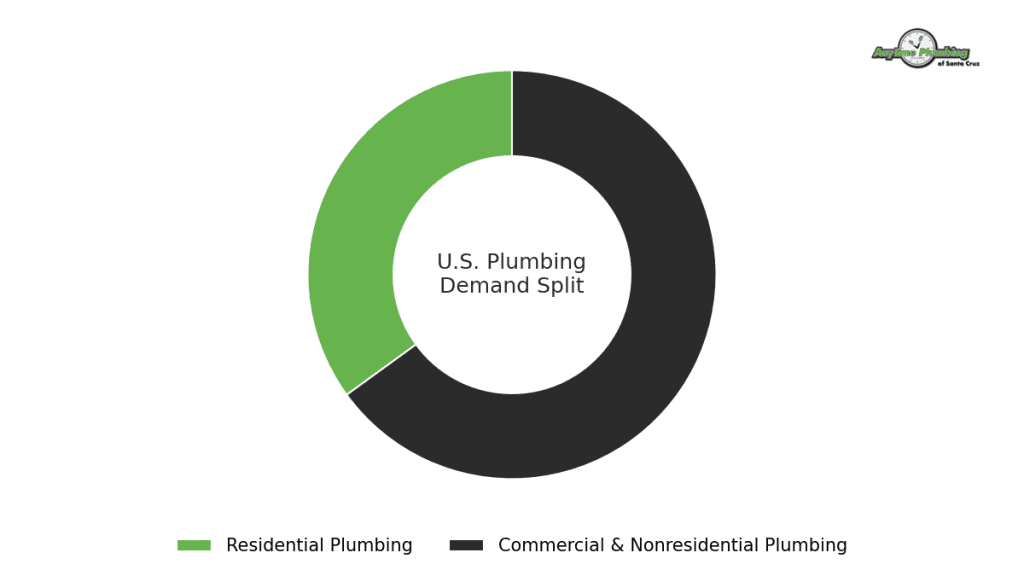

A combination of everyday residential needs and large-scale commercial activity drives demand for plumbing services in the United States. While homeowners generate a high volume of service calls, commercial projects account for a disproportionate share of total industry revenue.

Residential plumbing demand is largely maintenance-driven, covering repairs, replacements, and upgrades in existing homes. Commercial demand, by contrast, is tied to construction cycles, institutional facilities, and long-term infrastructure projects, resulting in higher average job values.

Key demand breakdown insights:

- Residential plumbing accounts for the majority of individual service calls, including leak repairs, water heaters, drain cleaning, and fixture replacements.

- Commercial and nonresidential plumbing represents the larger share of total industry revenue due to higher project scale and complexity.

- Multi-family housing, healthcare facilities, schools, and hospitality properties are major contributors to commercial plumbing demand.

- Residential demand remains stable year-round because plumbing repairs are typically non-discretionary.

- Commercial plumbing demand is influenced by construction activity, renovation cycles, and regulatory requirements.

- Aging residential housing stock continues to sustain strong demand for repair and retrofit services nationwide.

Average Plumbing Service Costs (Industry Benchmarks)

Plumbing service costs in the United States vary widely depending on job complexity, labor requirements, and urgency. Rather than a single fixed price, industry pricing is best understood through national cost ranges that reflect common service scenarios across residential and commercial work.

Labor remains the dominant cost driver for most plumbing services, while emergency response and specialized repairs significantly increase total job pricing. These benchmarks reflect industry-wide averages, not local or promotional rates.

Key plumbing cost benchmarks across the U.S.:

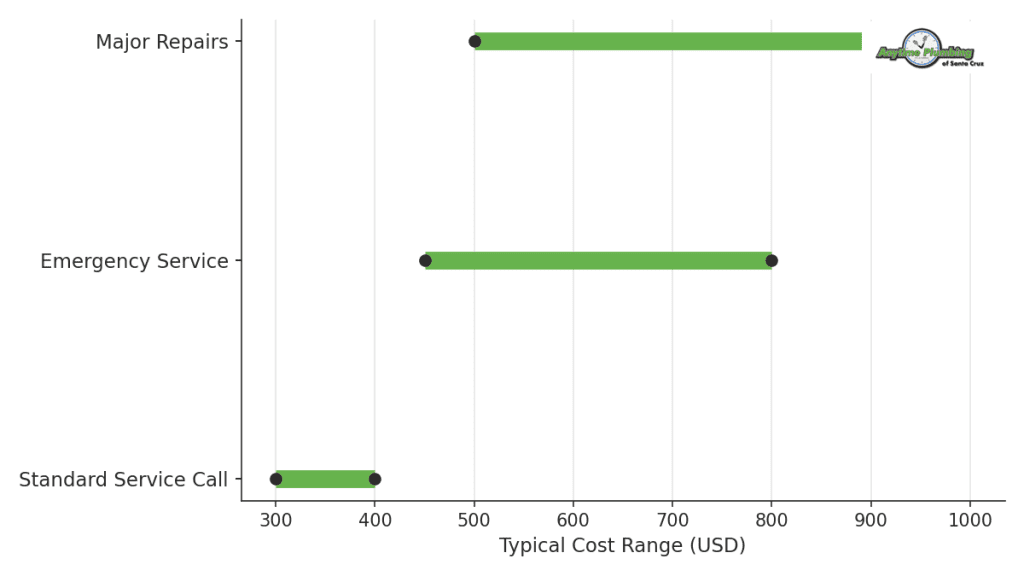

- The average plumbing service call typically falls between $300 and $400, covering labor, basic diagnostics, and minor repairs.

- Hourly labor rates commonly range from $75 to $150, depending on experience level and market conditions.

- Emergency plumbing services often cost 1.5× to 2× standard rates due to after-hours response and urgency.

- Small repairs, such as fixture replacements or minor leaks, frequently cost $150 to $350.

- Larger repairs, including water heater work, pipe replacements, or sewer-related services, commonly range from $500 to $1,000+.

- Commercial plumbing jobs generally carry higher average costs due to scale, permitting requirements, and system complexity.

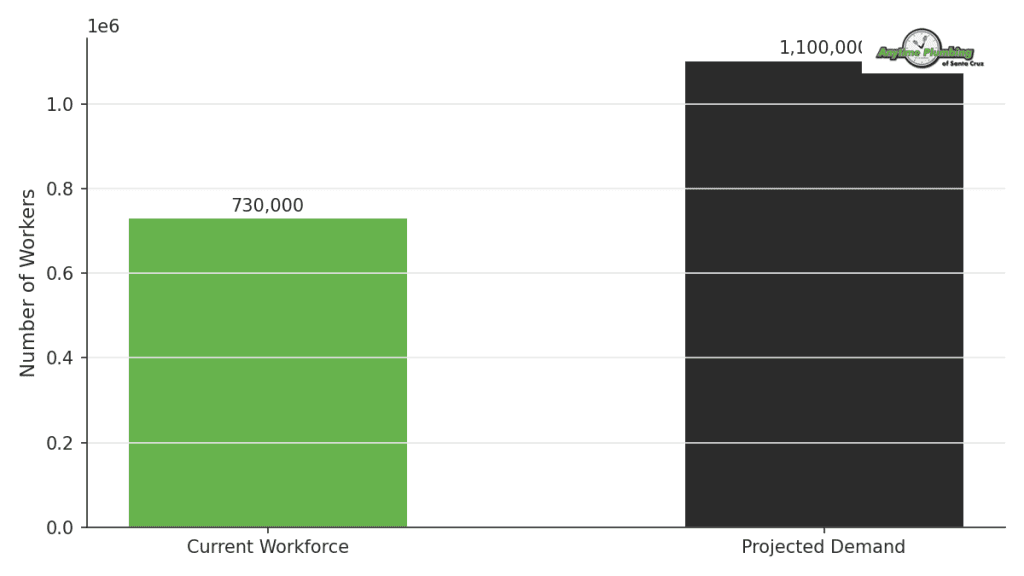

Plumbing Workforce & Labor Shortage

The U.S. plumbing industry relies on a large, skilled workforce, but labor availability remains one of the sector’s most pressing challenges. Despite steady demand for services, the number of qualified plumbers entering the trade continues to lag behind retirements and overall industry needs.

This imbalance between supply and demand affects service availability, project timelines, and labor costs across both residential and commercial plumbing markets.

Key workforce and labor shortage insights:

- The U.S. plumbing industry employs hundreds of thousands of skilled workers, including licensed plumbers, pipefitters, and apprentices.

- A significant portion of the workforce is approaching retirement age, contributing to long-term labor supply constraints.

- The number of new plumbers entering the trade has not kept pace with replacement demand, creating a persistent labor gap.

- Labor shortages place upward pressure on wages and service pricing, particularly in high-demand regions.

- Apprenticeship and trade training programs remain the primary pipeline for new workers, but enrollment levels are insufficient to offset workforce attrition.

- Workforce shortages are most acute during peak construction and renovation periods, amplifying scheduling delays.

- Limited labor availability has encouraged increased use of prefabrication, scheduling technology, and efficiency-focused workflows within the industry.

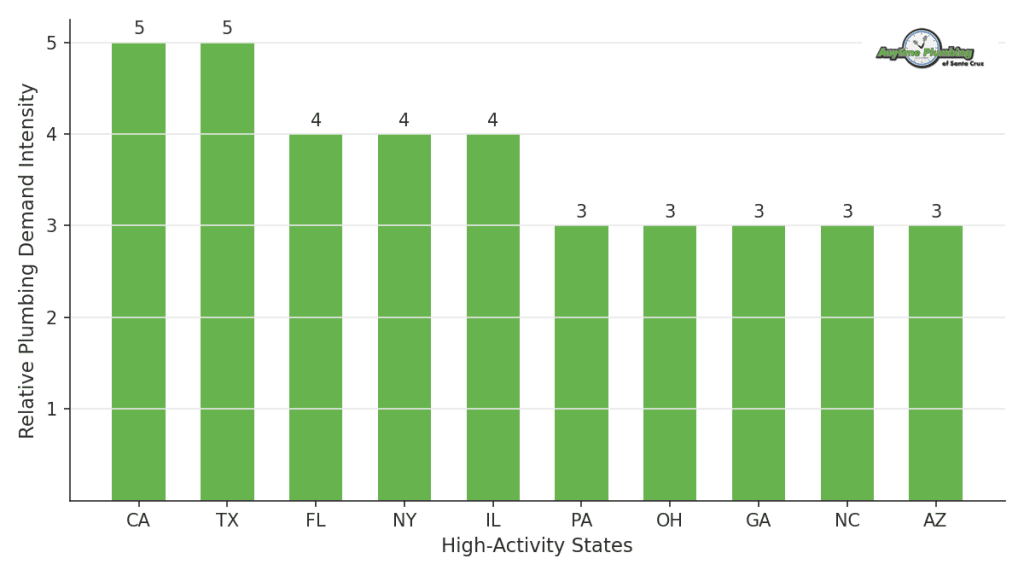

Regional Demand & Activity Hotspots (U.S.)

Plumbing demand in the United States varies significantly by region, influenced by population growth, construction activity, climate conditions, and infrastructure age. While plumbing services are essential nationwide, certain states and metropolitan areas consistently generate higher levels of activity.

High-growth regions tend to drive demand through new residential and commercial development, while older urban areas sustain steady work through system repairs, retrofits, and code compliance upgrades.

Key regional demand patterns across the U.S.:

- Large-population states generate the highest overall plumbing activity due to scale, housing density, and commercial infrastructure.

- Sun Belt states experience elevated demand driven by population growth, housing development, and year-round construction cycles.

- Older metropolitan regions sustain strong plumbing demand due to aging buildings, legacy piping systems, and frequent repair needs.

- Cold-weather regions see increased service volume related to freeze damage, pipe failures, and winter system stress.

- Areas with high concentrations of multi-family housing, healthcare facilities, and hospitality properties generate above-average commercial plumbing demand.

- Regional labor availability and wage levels influence service capacity and response times in high-demand markets.

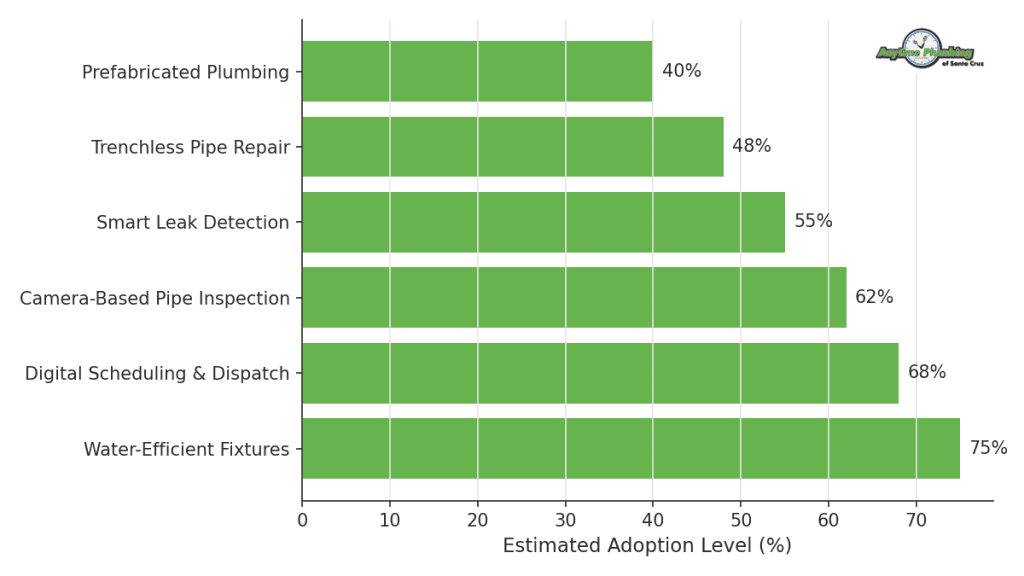

Plumbing Industry Trends & Technology Shifts

The plumbing industry continues to evolve as contractors adopt new technologies, materials, and service models to improve efficiency and meet changing customer expectations. Labor constraints, water-efficiency standards, and the increasing integration of digital tools across home services drive these shifts.

Rather than replacing traditional plumbing work, technology primarily reduces labor intensity, improves diagnostics, and modernizes system performance across residential and commercial applications.

Key trends shaping the plumbing industry:

- Innovative plumbing technology is increasingly used for leak detection, water monitoring, and system diagnostics, particularly in residential properties.

- Water-efficient fixtures and systems remain a significant focus due to conservation standards, utility incentives, and rising water costs.

- Trenchless repair methods are gaining adoption for sewer and pipe replacement, minimizing excavation and reducing project timelines.

- Digital inspection tools, including camera-based pipe diagnostics, improve accuracy and reduce unnecessary repair work.

- Plumbing contractors are adopting field service management software to streamline scheduling, dispatch, and invoicing.

- Prefabrication and modular plumbing components are increasingly used in commercial and multi-family construction to offset labor shortages.

- Customer expectations increasingly favor faster response times, transparent pricing, and digital communication, influencing service delivery models.

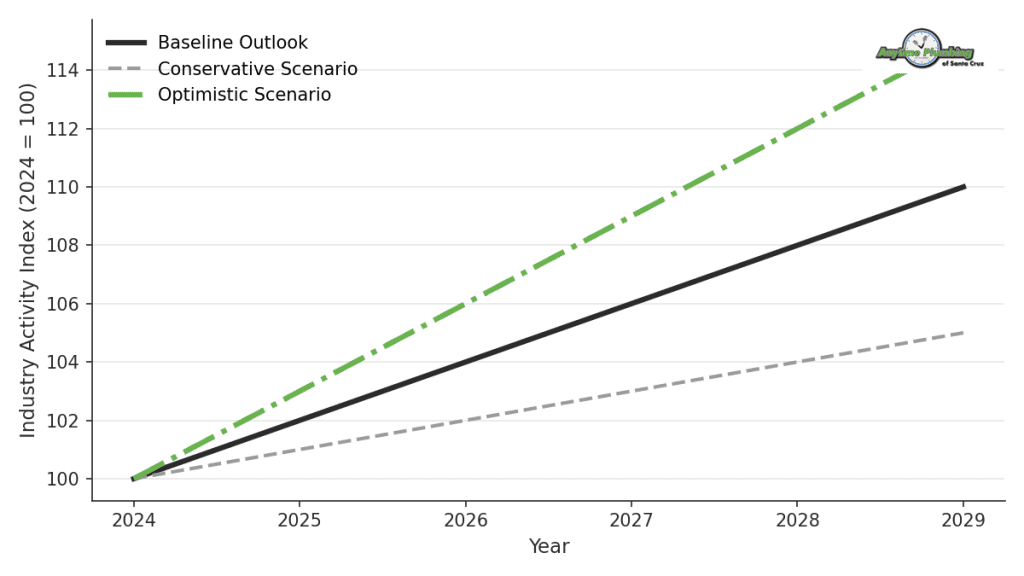

Future Outlook for the U.S. Plumbing Industry

The outlook for the U.S. plumbing industry remains stable, with demand supported by essential service needs rather than discretionary spending. Ongoing maintenance requirements, infrastructure replacement, and building modernization continue to anchor long-term activity across residential and commercial markets.

Rather than rapid expansion, the industry’s trajectory is shaped by steady service demand, labor availability, and efficiency improvements, with growth concentrated in select regions and service categories.

Key factors shaping the industry outlook:

- Plumbing services remain non-optional, ensuring consistent baseline demand regardless of broader economic cycles.

- Aging residential and commercial buildings continue to drive long-term repair and replacement activity.

- Infrastructure investment supports sustained demand for pipe replacement, system upgrades, and code compliance work.

- Labor availability is expected to remain a limiting factor, influencing service capacity and pricing dynamics.

- Technology adoption improves productivity but does not fully offset skilled labor shortages.

- Population growth and regional migration patterns influence where future demand is most concentrated.

- The industry favors operational efficiency and modernization over rapid workforce or capacity expansion.

Frequently Asked Questions

Demand for plumbing services has steadily increased due to population growth, aging infrastructure, and more homeowners investing in renovations. This trend is expected to continue as cities expand and plumbing technology evolves.

Industry data shows that a large portion of plumbing service calls involve urgent problems such as leaks, pipe failures, or sewer backups. Estimates suggest roughly 70 to 80 percent of plumbing jobs require quick attention, which explains why emergency plumbing services remain a major part of the industry.